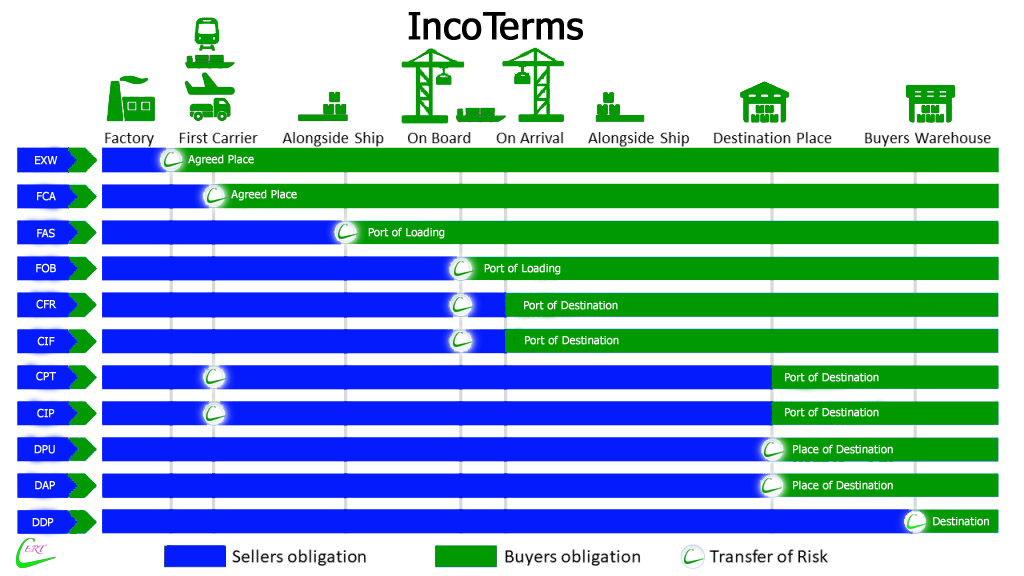

Delivered Duty Paid (DDP)

“Delivered Duty Paid” means that the seller delivers the goods when the goods are placed at the disposal of the buyer, cleared for import on the arriving means of transport ready for unloading at the named place of destination. The seller bears all the costs and risks involved in bringing the goods to the place of destination and has an obligation to clear the goods not only for export but also for import, to pay any duty for both export and import and to carry out all customs formalities.

Can be used for any transport mode, or where there is more than one transport mode.

The seller is responsible for arranging carriage and delivering the goods at the named place, cleared for import and all applicable taxes and duties paid (e.g. VAT, GST).

Risk transfers from seller to buyer when the goods are made available to the buyer, ready for unloading from the arriving conveyance

This rule places the maximum obligation on the seller, and is the only rule that requires the seller to take responsibility for import clearance and payment of taxes and/or import duty.

These last requirements can be highly problematical for the seller. In some countries, import clearance procedures are complex and bureaucratic, and so best left to the buyer who has local knowledge.

Delivered Duty Paid (DDP): Further information

In some countries, use of this rule is prohibited.

Some taxes such as VAT may only payable by a locally-registered business entity, so there may be no mechanism for the seller to make payment.

If the seller is willing to undertake the other obligations associated with import of the goods, then the rule may be qualified, e.g. Delivered Duty Paid (VAT unpaid).

For more details regarding the updated 2020 terms, please speak with your nominated shipping company or refer to the International Chamber of Commerce.

There are two key changes in Incoterms ® 2020 compared to the last edition:

- DAT (Delivered at Terminal) is renamed Delivered at Place Unloaded (DPU)

- FCA (Free Carrier) now allows for Bills of Lading to be issued after loading

Other changes include:

- CIF (Cost, Insurance and Freight) and CIP (Carriage and Insurance Paid To) set out new standard insurance arrangements, but the level of insurance continues to be negotiable between buyer and seller.

- Where listed, cost allocation between buyer and seller is stated more precisely – one article lists all costs the seller and the buyer are responsible for.

- FCA (Free Carrier), DAP (Delivered at Place), DPU (Delivered at Place Unloaded) and DDP (Delivered Duty Paid) now take account of buyer and seller arranging their own transport rather than using a third party.

- Security-related obligations are now more prominent.

- “Explanatory Notes for Users” for each Incoterm® have replaced the 2010 edition’s Guidance Notes, and are designed to be easier for users.

- CIP now requires as default insurance coverage ICC A or equivalent. It was ICC C under Incoterms® Required insurance coverage under CIF remains.